Rising Middle East tensions and policy uncertainty are driving a flight-to-safety, bolstering the U.S. Dollar while elevating energy-related inflation risks.

Escalation of Middle East Conflict

The geopolitical landscape in the Middle East has entered a period of acute instability following the effective collapse of the U.S.-Iran memorandum of understanding (MoU). In response to ongoing Iranian efforts to force commercial vessels through an illegal traffic separation scheme, the U.S. and its allies have engaged in a series of direct military confrontations. Tensions have peaked with Iranian military strikes on tankers in the Strait of Hormuz, countered by U.S. and Israeli military operations aimed at degrading Iranian infrastructure. As Iran attempts to leverage control of the strait to secure concessions, the region remains trapped in a volatile cycle of military posturing and retaliatory strikes, with little immediate prospect for a durable political settlement.

Flight to Safety and USD Dominance

Financial markets have reacted to this heightened friction with a swift movement toward safe-haven assets, reinforcing the dominance of the U.S. Dollar. As uncertainty ripples through global trade networks, investors have prioritized liquidity and stability, shunning risk-sensitive equities in favor of Treasury bonds and gold. The maritime blockade in the Strait of Hormuz—a vital chokepoint for nearly 20% of global oil supplies—has acted as the primary catalyst for this shift, causing extreme volatility and driving up insurance and shipping costs globally. The resulting market climate reflects a broader anxiety as institutional capital retreats from exposure to regions vulnerable to the direct impact of the conflict.

Macro-Economic Pressure and Inflationary Concerns

The global economy is currently navigating a period of profound structural strain characterized by surging energy costs and the specter of stagflation. The supply disruptions linked to the conflict have forced central banks to reconsider their monetary trajectories, with many postponing interest rate reductions to contend with rising inflation. Beyond the immediate volatility in oil markets, there are growing concerns regarding food security and industrial output, as businesses across the EU and North America face steep surcharges for electricity and raw materials. These pressures are coalescing into a long-term challenge, as nations realize that their dependence on vulnerable energy routes poses an existential risk to their economic resilience, potentially prompting a permanent shift in trade and investment strategies.

Top upcoming economic events:

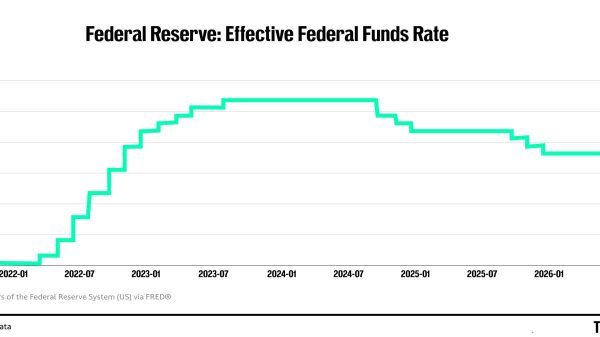

07/08/2026 – FOMC Minutes The release of the Federal Open Market Committee minutes is arguably the most critical event of the week for the U.S. dollar and global equity markets. Investors closely scrutinize these documents for nuanced details regarding the committee’s deliberation on interest rate trajectories, providing insight into whether the Federal Reserve remains concerned about inflation or is shifting toward a more supportive stance for growth.

07/08/2026 – EIA Crude Oil Stocks Change This U.S. energy report provides a snapshot of domestic crude supply levels. Because energy costs are a major input for businesses and a significant factor in consumer inflation, unexpected shifts in stockpile data often trigger immediate volatility in oil prices and energy-sensitive sectors.

07/08/2026 – 10-Year Note Auction As a benchmark for long-term borrowing costs, U.S. Treasury auctions are vital for fixed-income markets. The demand at this auction—measured by the bid-to-cover ratio and yields—serves as a key indicator of investor confidence in U.S. debt and influences broader mortgage rates and corporate bond yields.

07/09/2026 – China Consumer Price Index (YoY) China is a critical engine for global economic health. Inflation data from the world’s second-largest economy acts as a bellwether for consumer demand. High readings suggest robust internal consumption, while low or negative readings often raise concerns about economic stagnation in the region and weakened global trade.

07/09/2026 – China Producer Price Index (YoY) Released alongside the CPI, the PPI provides essential data on factory-gate price pressures in China. Because China is a major manufacturing hub, these figures offer early signals regarding global supply chain costs and can directly impact the profitability expectations of multinational corporations that rely on Chinese production.

07/09/2026 – U.S. Initial Jobless Claims This weekly report is one of the most timely indicators of the strength of the American labor market. A sharp increase in claims can signal a softening economy, while a decline suggests persistent tightness in the job market, both of which are major drivers of Federal Reserve policy expectations.

07/09/2026 – U.S. Existing Home Sales This report tracks the volume of previously owned homes sold, serving as a significant proxy for consumer confidence and housing market health. Since housing is a massive contributor to the U.S. economy, these numbers help investors gauge the impact of current mortgage rates on the average American household.

07/09/2026 – 30-Year Bond Auction The 30-year bond auction is a high-stakes event that signals long-term investor sentiment regarding U.S. fiscal health and future inflation expectations. Yields from this auction are often used to price long-term capital investments, making them a primary focus for institutional investors and pension funds.

07/10/2026 – Eurozone Harmonized Index of Consumer Prices (YoY) The HICP is the European Central Bank’s preferred measure of inflation. Given the ongoing debates regarding monetary policy in Europe, this data point is pivotal; it helps the market determine whether the ECB needs to maintain higher rates to combat inflation or if it has space to provide economic stimulus.

07/10/2026 – UK NIESR GDP Estimate The National Institute of Economic and Social Research (NIESR) GDP estimate provides an independent, up-to-date look at the UK’s economic momentum. As a three-month tracking metric, it is highly valued by analysts looking for early warning signs of recession or acceleration before official government data is released.

The subject matter and the content of this article are solely the views of the author. FinanceFeeds does not bear any legal responsibility for the content of this article and they do not reflect the viewpoint of FinanceFeeds or its editorial staff.

The information does not constitute advice or a recommendation on any course of action and does not take into account your personal circumstances, financial situation, or individual needs. We strongly recommend you seek independent professional advice or conduct your own independent research before acting upon any information contained in this article.