Wall Street’s careening trajectory has left investors grappling with a highly volatile macro climate.

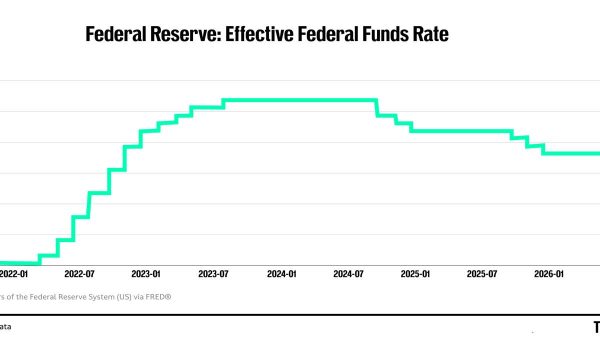

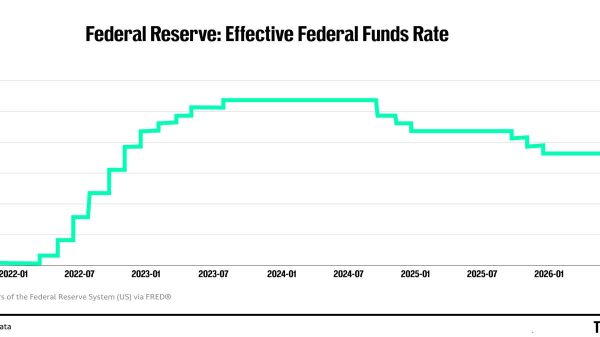

Despite brief relief from a tentative US-Iran ceasefire, the Federal Reserve’s latest Summary of Economic Projections paints a hawkish picture – slashing GDP expectations while projecting sticky PCE inflation at 3.6%.

With newly appointed Fed Chair Kevin Warsh signaling that interest rates will remain “higher for longer” and keeping a 2026 rate hike firmly on the table, hyper-growth sectors face sustained pressure.

When structural inflation and policy uncertainty cloud the horizon, cash flow is king.

Navigating this choppy backdrop requires anchoring a portfolio in rock-solid, defensive cash generators that balance market turbulence with reliable yield.

Irrespective of where the broader market heads next, three iconic dividend powerhouses offer the ultimate defensive blueprint for resilient income: Altria, Walmart, and Coca-Cola.

Altria Group (MO)

Tobacco may be in structural volume decline across the US – but Altria Group Inc has forged one of the market’s most paradoxically durable income stories.

MO has raised its dividend for 56 consecutive years, currently yielding “6.15%”, an uncommon payout for an investment-grade income stock.

Nicotine’s addictive properties afford pricing leverage few consumer categories can replicate, which is why the company’s payout ratio stands at about 75% of 2026 earnings estimates – a serviceable level that leaves capacity for further hikes.

As cigarette volumes contract annually, Altria offsets the pressure through disciplined cost reduction and consistent price increases on its Marlboro-led portfolio.

For MO, Wall Street analysts project low- to mid-single-digit annualized earnings growth, sufficient to sustain the dividend’s upward trajectory for the foreseeable future.

Walmart (WMT)

Walmart – the world’s largest retailer brings an operational moat of almost incomprehensible scale to the dividend equation.

With roughly 90% of the US population living within a short drive of a Walmart store, the company holds a captive consumer base spanning grocery, general merchandise, pharmacy, and automotive services, often under a single roof.

That physical density, combined with supplier leverage derived from WMT’s purchasing volume, enables sustained low-price leadership that competitors cannot match at equivalent margins.

Walmart has raised its dividend for 53 consecutive years, and analysts project 9% to 10% annual earnings growth over the next three to five years, driven by accelerating e-commerce penetration and an expanding retail media advertising business.

So, the dividend, by any structural measure, faces minimal risk.

Coca-Cola (KO)

There aren’t a lot of businesses that can replicate the earnings consistency of Coca-Cola.

The company sells more than 2.2 billion product servings daily across a portfolio extending well beyond its flagship cola, encompassing water, juice, coffee, tea, and energy drinks, distributed through virtually every commercial channel globally.

That volume underpins a 64-year dividend growth streak, the longest among the three names profiled here, with a current yield of 2.65%.

Analysts project at least 7% compound annual earnings growth over the next three to five years, supported by price and mix improvements alongside geographic diversification across developed and emerging markets.

Perhaps the most durable endorsement: Warren Buffett’s Berkshire Hathaway has held Coca-Cola stock continuously since the late 1980s – an institutional conviction that, across four decades, has proven well-placed.

The post Three must-own dividend stocks irrespective of the broader market trajectory appeared first on Invezz